DPC Myth #21: Adding DPC to any employer health plan will automatically save on health insurance premiums

When employers and DPC doctors start talking, the obvious elephant in the room is the question: “Does this save money?” The simple answer is “Yes…but”.

There are complications to this question that must be addressed up front. It matters how an employer’s health plan is structured, and it matters how DPC is positioned within that structure.

If the employer you’re working with pays for a “BUCA” plan (a health plan administered in whole or in part by Blue Cross, United Healthcare, Cigna, or Aetna), then you need to hold back on any assertions that DPC will save money in that environment.

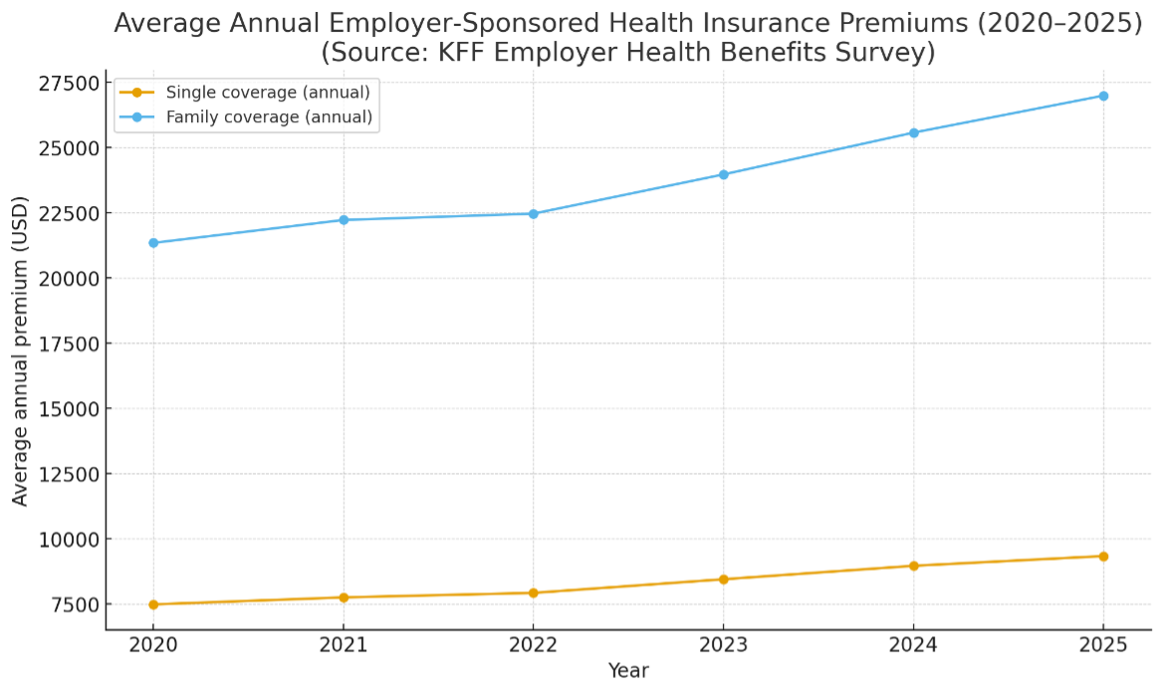

Exhibit A – This chart shows the Kaiser Family Foundation’s documented increases in both single and family coverage over the last 5 years. Almost all these data points come from BUCA plans. As you can see, there are NO savings in this environment, and none are predicted soon.

Here’s another point to consider…the BUCAs cannot lower their premiums…EVER! That would be contrary to their business model and would be a breach of fiduciary duty, which requires them to return profits to their shareholders. The BUCAs do not have a fiduciary duty to their customers. That question was even argued in court in Massachusetts. The judge, as well as the Court of Appeals, agreed that BCBSMA was NOT a fiduciary to the Massachusetts Laborers’ Health & Welfare Fund, which was suing them overpaying providers’ amounts exceeding the rates previously negotiated (i.e., overpaying claims), failing to recover overpayments properly, and withholding information necessary for the Fund to verify correct pricing.

So, this chart should adequately prove that the BUCAs’ only allegiance is to their shareholders. In case the legend is too small, the blue line represents Elevance (BCBS plans across the country), the yellow line represents United Healthcare, and the red line represents Cigna. The green line represents Humana (no longer in the employer market), and the black line is the Dow Jones Industrial Average for comparison.

Lastly, BUCAs are in the business of vertical integration. Stop calling them “insurance companies”. They don’t even call themselves that anymore. They call themselves “healthcare services organizations”. So, they believe their job is to use profits to buy up as many healthcare services as possible, thereby owning the entire healthcare journey, including primary care.

Please don’t take offense at the following statement. I only mean for it to save you time and trouble. But, knowing all this, no DPC practice can move the needle on costs in this environment. DPC does not belong within a country mile of a BUCA employer-sponsored group plan. You’re simply outmanned and outgunned.

One recent caveat to this is, of course, the innovation coming up on 1/1/2026 courtesy of the OBBBA. That is, if an employee or individual healthcare purchaser has a qualified high-deductible health plan and contributes money into an HSA from which they can pay for your DPC services…then great, that’s one example of how DPC might work in a BUCA environment. But, honestly, it’s not a great fit, and I think you’ve probably already experienced that when working with patients who have traditional health insurance.

How health plans are structured matters. That’s why groups like Health Rosetta, Free Market Medical Association, Mitigate Partners, and others advocate for employer health plans independent of the BUCAs, with the freedom to build group plans that place DPC at the foundation of high-performing plans that yield much better outcomes.

Here’s wishing you a wonderful holiday season! Stay healthy, Y’all!

Great post! In my experience, good DPC practices reduce the health risk of the employee population, Mostly due to better chronic condition management. Employers must mandate or provide incentives for DPC usage or dis-incentive non-DPC usage. Short term cost can go up, and often do. But Long term costs of those participating in the DPC plan tend to go down. Black Swan events, like cancers, premie babies and emergency care will always remain. Most DPC providers do not have sufficient cost, and quality data to steer to higher value doctors And work best when paired with a patient advocacy Company that has this information

see https://dpcnews.com/opinion/fear-will-remove-the-d-in-dpc/

I am confused. I thought the BUCA plans were non-profit and did not have shareholders? So Blue Cross/Blue Shield has to keep raising prices because of their shareholders?