“ICHRAs = Health Plan Simplicity + DPC”

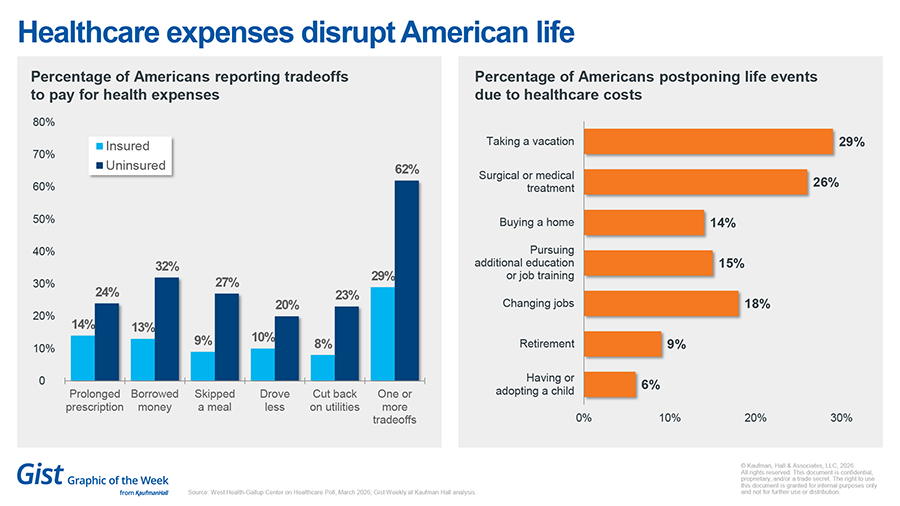

With many primary elections in the past and the November general elections ahead, we’re going to be seeing healthcare in the headlines more frequently than ever. There’s no denying we’re seeing a tipping point like never before. More employers are seeking alternatives to how they’ve been paying for their employees’ healthcare. More patients/individuals/employees are speaking up about the plans their employers are choosing that are supposed to benefit them. The infographic above illustrates the measures American families are taking to cope with rising healthcare costs in the traditional system.

Last month, I wrote about alternative funding strategies such as level-funding and self-funding. This month, let’s talk about a rising trend called ICHRAs. That stands for Individual Coverage Health Reimbursement Arrangements. It’s where an employer contributes to a special health reimbursement arrangement (HRA) that provides a monthly or annual stipend employees can use to pay for individual coverage on the marketplace. In some ICHRA setups, if money remains after the individual plan is purchased, the remaining stipend can be used for out-of-pocket healthcare expenses listed in section 213(d) of the Internal Revenue Code.

According to the interpretation and guidance on Dr. Phil Eskew’s website, HRAs and FSAs have always been able to reimburse DPC membership fees, as well as incidental fees a patient might incur at the direction of their DPC physician.

The newest and most innovative ICHRA platforms also include access to health sharing plans that employees can choose from. To be clear, a contribution to a health sharing plan cannot be accessed through the HRA itself, and if the employer pays the monthly membership fees associated with health sharing plans, it must be done on an after-tax basis.

However, combining those choices into a single platform, helping employees navigate and enroll in their desired options, and structuring payments so that the right contributions go to the right vendors each month are some of the newer capabilities of emerging ICHRA platforms. This newer structure gives employees more choice, better guidance, and can lead to greater uptake of DPC-friendly plans.

A smart strategy could look like this:

- Employer offers to pay 100% of a health sharing option plus a DPC membership for the employee. This choice (depending on the employee’s age) is usually way more affordable than an individual plan on the ACA marketplace.

- OR, for employees who need “insurance”, the employer offers to pay an average stipend that would likely purchase a Bronze Plan on the ACA marketplace. This opens the option of adding a health savings account (HSA), which can now also be used to pay for DPC memberships. Each group’s census should be used to determine the average stipend based on factors such as employee age, zip code, and salary.

- If the employee wants a richer plan or they want to cover dependents, then they pay the difference through payroll deduction.

- ICHRA strategies executed properly absolve the employer from risk of penalties associated with the “employer mandate” as it meets “minimum essential coverage”. These are requirements for employers with more than 50 eligible employees, under the PPACA (also known as the Affordable Care Act or Obamacare).

In summary, some employers have told me they want to get out of the “insurance business” and just give employees money so they can choose their own health insurance. I can certainly respect that and agree that for some employers, maintaining a group health plan can be a headache they’re happy to leave behind.

Using more modern ICHRA strategies can help employers strike the right balance while also guiding employees toward your DPC practice.