Let’s Pretend Health Insurance is Auto Insurance

Have you ever had a minor vehicle “bump up” and decided to handle it yourself without filing a police report or an auto insurance claim? Surveys suggest 35% of the 20+ million drivers in the US have had a minor accident and decided NOT to file a claim with their auto insurer, according to Lending Tree, a US-based online financial marketplace.

Why would this behavior exist? Don’t we all want to “get our money’s worth” out of the products and services we purchase? Of course, but the learned response we’re identifying here is because of a negative outcome to filing insurance claims for “covered services” that didn’t need to be insured in the first place. I bet this analogy sounds familiar. It’s the same mantra we’ve been putting forth as part of the logic behind direct primary care since it began.

The way I’ve been saying it to employers lately is, “Every care encounter your employee has with the healthcare system does not need to be insured, and if your plan is self-funded and administered by a BUCA (Blue Cross/Blue Shield, United Healthcare, Cigna, Aetna), then you want as few claims paid by them as possible”. Indeed, every time a BUCA receives, consumes data for, and then pays a claim to any provider, that’s a win for them and a loss for the employer plan and the provider. However, that employer’s loss isn’t realized immediately. It usually flies under the radar until their subsequent renewal increase (just in time for them to have no recourse).

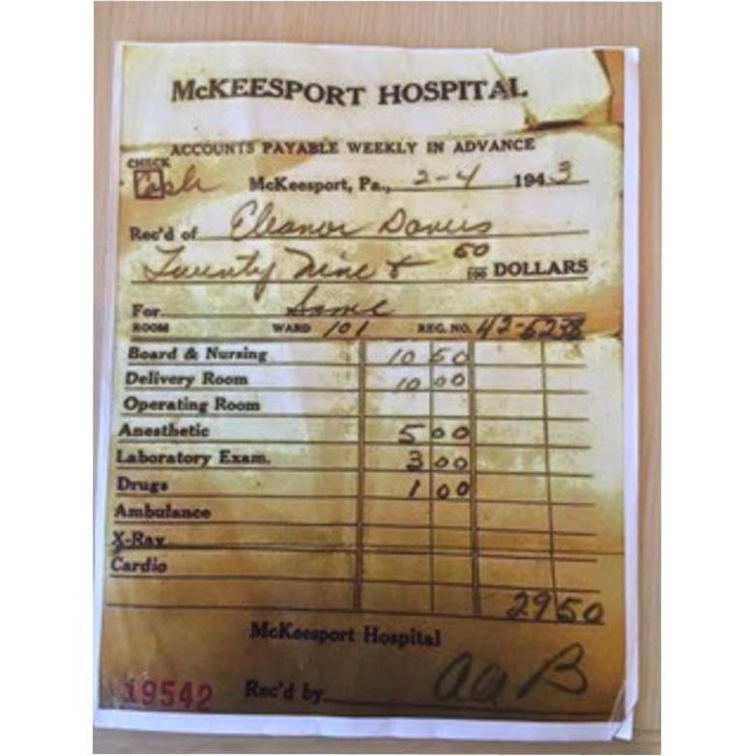

You may be scratching your head here and asking, “If a claim is paid, isn’t that automatically a loss for the carrier?” Not exactly, and here’s how…let’s take a claim that happens nearly 10,000 times every day in America – a baby is born. Here’s a snapshot of a labor and delivery charge back in the good old days before BUCAs existed:

Today’s itemized hospital bills can be dozens of pages, with hundreds of codes, and astronomical prices for the same type of simple labor & delivery depicted in that old photo.

It’s important to remember here that when BUCA plans are involved, in most cases, the higher the starting price, the better for the BUCA. That’s counterintuitive to most people. Here’s why: BUCAs exist because they use two sets of contracts to administer a health plan.

One contract is between them and the employer. The other contract is between them and their network providers. The difference between those contracts is the margin that the BUCA keeps in its pocket.

Here’s a made-up example: let’s say an employee has a primary care visit, and the starting price is $300. When the provider joined the network, they agreed to a specific discount. Let’s say that’s around 60% to start with (it’ll change over time in favor of the BUCA). After the charge is discounted, the allowed amount is $120. The BUCA may deduct $120 from the employer’s claims account, but then only “reimburse” the provider $60. That leaves a $60 margin that the BUCA keeps for itself. This happens every time a BUCA processes a claim.

So, you already know these games…but the employers near you don’t. They think BUCAs pay claims, and the premiums associated with that plan are 100% of their revenue. Nope! Not even close. It’s estimated that BUCAs have dozens of different revenue streams.

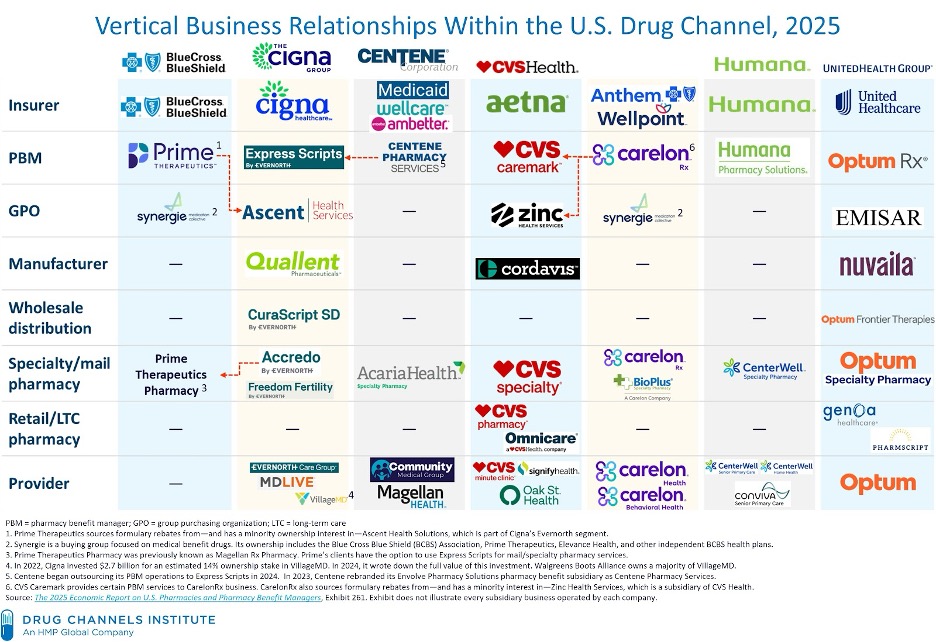

And with vertical integration (see the familiar chart below that I use often), they get to keep even more money, especially through their integrated pharmacy benefits manager and (in some cases) pharmacies they wholly own.

If you really want to get your heart rate up, read this expose’ by Dr. Seth Glickman about what happens when a patient covered by Aetna takes a prescription for Imatinib to a CVS Pharmacy. Pretty infuriating!

Hint: stop asking patients where they “want” their prescriptions sent. Instead, ask them if they know their local community pharmacist. If the answer is “No”, make the introduction. Everyone needs a local, independent, community pharmacist on their local care team. It’s just practicing good medicine.

In 2026, let’s work to educate the employers in your area so that they more clearly understand how they are getting taken advantage of and how they can stop the bleeding.

If you celebrate Christmas, I want to wish you a Merry Christmas. If you celebrate something else, Happy Holidays!